Credit Management Mastery: How Aria Empowers Your Risk Strategy

What’s the secret to staying ahead of credit risks? Marie Cressiot shares how Aria’s 3-pillar strategy protects your cash flow and powers your growth.

Insights from Marie Cressiot, Risk Manager at Aria.

Over my six years in Risk Management roles, I’ve often seen companies underestimate the credit risks posed by their clients. When growth is the primary focus—and especially if you’re not in the financial sector—credit risk can feel like a distant concern. Unfortunately, it is usually only when the consequences hit—therefore too late—that companies realize the importance of having a strong risk management framework in place.

But it doesn’t have to be this way. In this article, I’ll share how Aria helps you stay ahead of credit risk, so you can protect your business and focus on what you do best: growing with confidence.

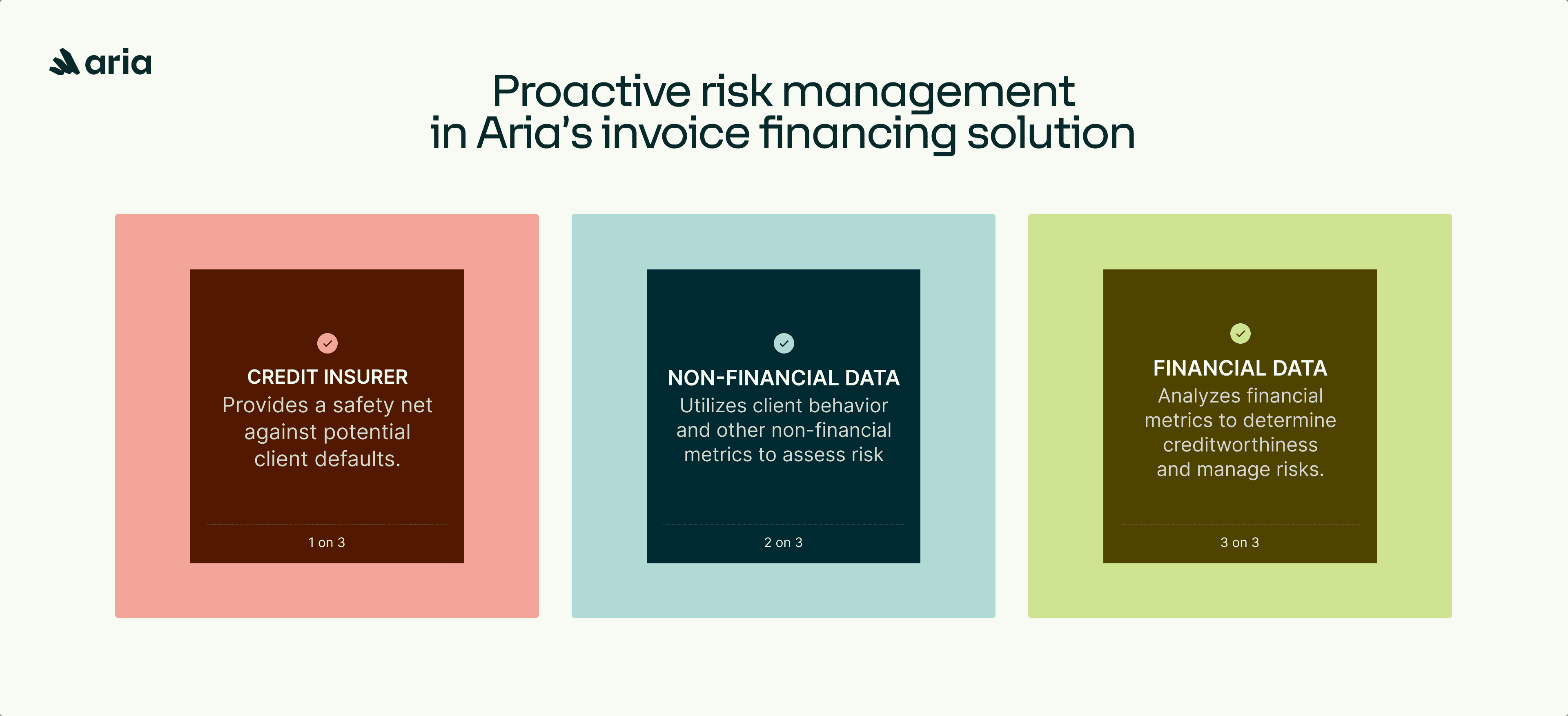

The 3 pillars of Aria’s risk management

At Aria, we provide an embedded invoice financing solution. In simple terms, it’s factoring directly integrated into a platform. This makes managing debtor risks—clients failing to pay—an essential part of what we do. While this challenge is largely statistical, we’ve developed a methodology that ensures we’re not just responding to risks but proactively managing them. Here’s how we approach it.

1. Our Credit Insurer

The first pillar of our risk management strategy is our partnership with our credit insurer, a global leader in the industry. Their expertise, and especially their international geographical coverage, enables us to access reliable ratings for almost every company around the world. At Aria, our debtors are located across Europe, the United States, Singapore, and the Middle East, so having access to accurate ratings that model the probability of default is essential to our risk management process.

But we don’t stop there. To avoid depending on a single data source, we also gather both financial and non-financial data through external providers. This way, we can build a more complete and nuanced risk scoring, tailored to Aria’s business and operations.

2. Non-Financial Data

We primarily use open-source platforms like Pappers or North Data to look beyond numbers and gather insights into a company’s legal structure, industry and history. For example, a newly founded business carries more risk than a business that has been around for 20 years, because there’s less data to analyze. Some industries, such as automotive, retail or construction, are inherently riskier due to the current economic situation.

This broader view helps us understand the context behind a company’s financial health, ensuring our evaluations are both accurate and well-informed.

3. Financial Data

Finally, through partnerships with specialized providers, we access detailed financial statements and key ratios to assess a debtor’s stability and repayment capacity in the short run. Our providers also supply us with key information about payment incidents. This data is highly valuable for assessing a debtor’s short-term solvency.

Together, these layers of data allow us to refine the ratings from our insurer and create an internal methodology that’s tailored to Aria’s specific needs.

Categorizing our debtors

All this data flows into our internal database, where it becomes the foundation for actionable insights.

My role as Risk Manager is to create methodologies that transform this raw data into more actionable and useful information—like categorizing companies based on their revenue and balance sheet size.

These insights feed into our decision tree, which is central to our processes. It doesn’t just calculate risk but guides us in making decisions about whether to finance a debtor.

For most cases (80–90%), this system provides quick answers. For the remaining 10–20%—the more complex situations—we dive deeper with manual analysis to ensure we’ve considered every angle.

Modeling financing limits

Once we decide to finance a company, the next step is determining how much risk we’re willing to take.

Based on our appetite for risk, we set the maximum amount we’re willing to advance to a company. This limit reflects our ability to absorb a potential default without jeopardizing our overall financial balance. While the risk score plays a role in pricing, it’s just one piece of the puzzle. Our Head of Finance has established minimum thresholds that account for both the risk level and other influencing factors.

That said, our appetite for risk is not fixed: it can evolve over time, based on new information about a company or developments in its sector. This agility allows us to respond to market changes and make well-informed, balanced decisions.

At Aria, credit management isn’t just about crunching numbers or mitigating risk. It’s about building trust and creating a system that protects your business while supporting growth. By combining credit rating from our insurer with both non-financial and financial data, as well as our expertise, we’ve developed a process that helps you reduce defaults and protect your financial stability. Beyond that, it provides you with valuable insights into your business partners’ situations – having insights into a major customer’s potential insolvency is invaluable.